.avif)

Persian Gulf crude oil exporters face a fundamental shift in margin structures as the UAE's offensive strikes against Iranian energy infrastructure have transformed war risk premiums from temporary volatility into embedded operational costs. Brent crude futures traded near $95-97 per barrel this week after falling from recent highs above $105/barrel as hopes for diplomatic progress briefly emerged. War-risk insurance has surged to about 4 per cent of a ship's value for seven days, vastly above pre-crisis levels of around 0.001 per cent. For a 2 million barrel VLCC (Very Large Crude Carrier a supertanker carrying crude oil worth approximately $190 million at current prices), that translates to $4 million in additional insurance costs per transit versus $1,900 pre-conflict. The arbitrage windows that once made Persian Gulf crude competitive in Asian markets have narrowed to the point where smaller regional traders are priced out entirely.

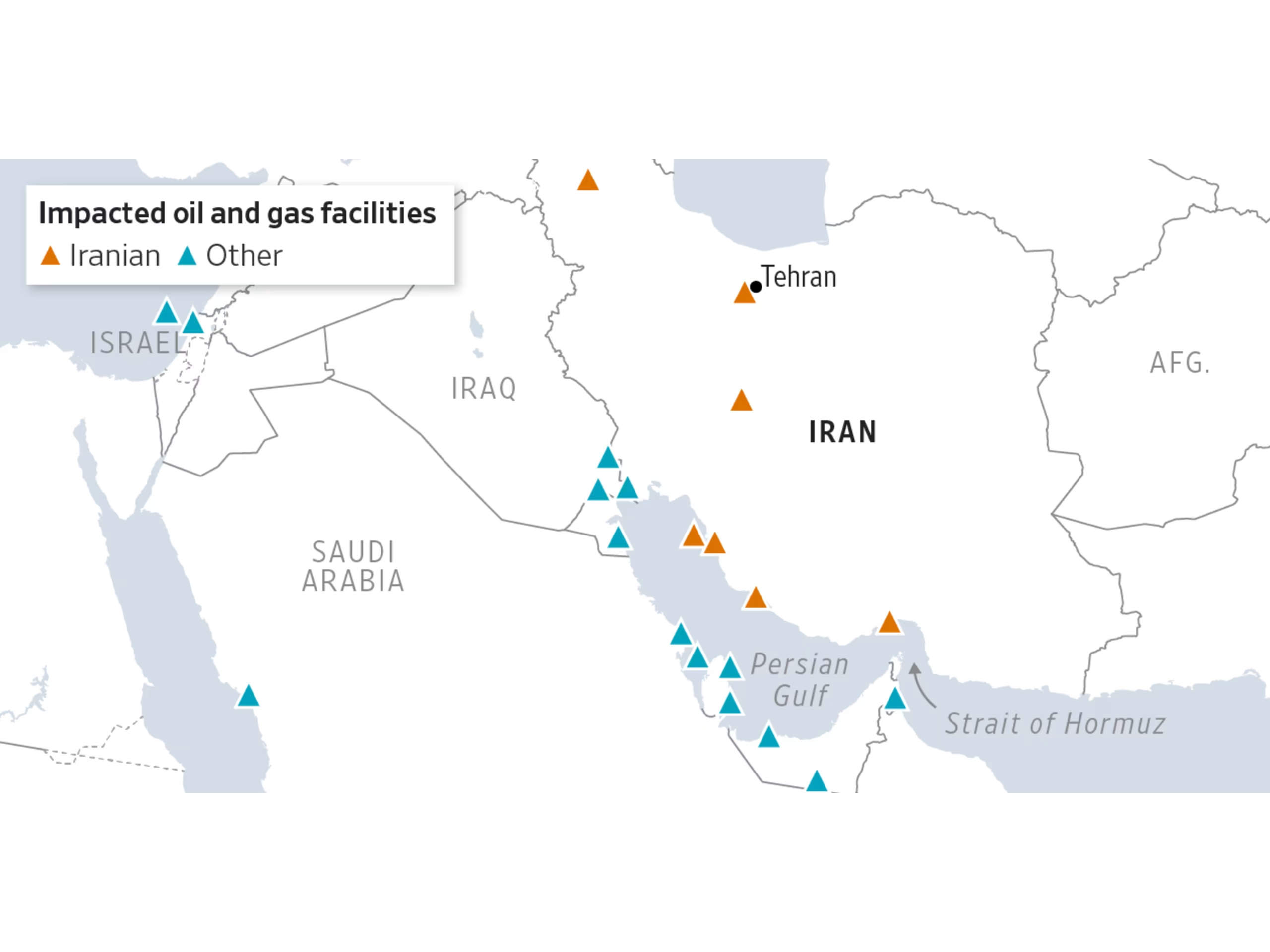

According to the Wall Street Journal, the UAE responded with strikes on Iranian infrastructure using warplanes and drones in coordination with the U.S. and Israel, which included the Lavan Island attack. The reported Emirati strike against Iran's Lavan Island refinery demonstrated that Abu Dhabi has shifted from a primarily defensive counter missile posture into direct offensive operations employing advanced Western supplied combat aircraft, surveillance assets, and precision strike capabilities against Iranian infrastructure. This escalation follows the UAE intercepting and destroying 537 ballistic missiles, 2,256 drone attacks and 26 cruise missiles fired from Iran using their THAAD and Patriot missile defence systems. The operational significance lies not in individual strikes but in the systematic targeting of refining capacity Lavan Island's 400,000 barrels per day refinery processes Iranian crude destined for regional and Asian markets. When refineries become legitimate military targets, the geographic concentration of Persian Gulf processing capacity becomes a strategic vulnerability rather than an efficiency advantage.

The Strait of Hormuz is a chokepoint in global energy supply chains, with roughly 20% of global oil supply transiting the passageway, including more than 40% of China's crude oil imports. Traffic has reportedly reduced by about 95% since the onset of the war. The combined capacity of alternative pipelines the East–West Crude Oil Pipeline to Yanbu and the Abu Dhabi Crude Oil Pipeline to Fujairah is about 9 million barrels per day, less than the roughly 20 million barrels per day that can pass through the strait. The mathematics are stark: even if every available pipeline operates at maximum capacity, two-thirds of Persian Gulf export capacity requires Strait of Hormuz transit. Reports claim anywhere between 30 and 70 vessels have crossed the strait some with US military guidance and even helicopter escorts since early May. They have faced the triple threat of Iranian sea mines, missiles and fast attack boats. Each escorted convoy represents an exception proving the new rule: routine commercial transit has ceased.

On the buy side, Asian refineries dependent on Persian Gulf crude face input cost increases of $15-20 per barrel beyond benchmark pricing, forcing operational adjustments across their entire slate. Chinese independent refineries often called "teapots" for their smaller scale that traditionally arbitrage Iranian crude against domestic production quotas find their margin structure entirely disrupted. Short-term container shipping freight rates have jumped all over the globe due to the Strait of Hormuz blockade: average spot rates in June are expected to be 75 per cent more from China to the US East Coast, 51 per cent higher to North Europe, 45 per cent to the Mediterranean and 57 per cent on the transatlantic from North Europe to US East Coast. Japanese and South Korean refineries with long-term supply contracts from Saudi Aramco or ADNOC (Abu Dhabi National Oil Company) benefit from contractual protection but face higher spot crude costs for incremental volumes and processing margin compression as product prices lag crude cost increases.

On the sell side, Persian Gulf national oil companies with alternative export infrastructure capture the largest margin expansion. The Habshan–Fujairah pipeline enables a significant share of Abu Dhabi crude exports to reach the Gulf of Oman without transiting the Strait, reinforcing the country's role as one of the region's most resilient suppliers during periods of geopolitical tension. ADNOC can effectively charge a $15-20 per barrel premium for Fujairah delivered crude versus Strait dependent competitors. Saudi Aramco benefits from similar optionality through its East-West Pipeline to Yanbu, though the Red Sea route is also vulnerable to possible Houthi attacks. Qatar faces the most constrained position its North Field condensate and LNG exports have no alternative to Strait transit, forcing QatarEnergy to either accept higher shipping costs or reduce production. The strategic premium now accrues not to the lowest-cost producer but to the most diversified exporter.

For large integrated traders with global footprints Vitol, Trafigura, or trading arms of national oil companies the disruption creates both margin opportunity and capital intensity pressure. The DFC announced it would partner with leading US insurers to establish a reinsurance facility providing up to $40 billion in coverage on a revolving basis, spanning hull, cargo, and liability risks. Access to US government backed war risk insurance becomes a competitive advantage, but only for traders willing to accept US oversight of their vessel movements and cargo destinations. The operational model shifts from spot optimisation to relationship dependent access. Derivatives markets offer limited protection: ICE Brent futures reflect supply disruption pricing, but there are no liquid instruments to hedge against transit-specific war risk premiums. Large traders hedge through portfolio diversification increasing exposure to Atlantic Basin crude, West African production, and US shale while maintaining Persian Gulf relationships for post-conflict positioning.

For smaller regional operators independent fuel importers, coastal refineries, or specialist product traders the current environment effectively eliminates Persian Gulf sourcing optionality. A mid-sized Indian refinery that previously balanced crude purchases between Saudi Arabia and Iraq based on monthly pricing now faces binary choice: pay the war risk premium or source entirely from non-Persian Gulf suppliers. Insurance is available but often at levels that make transits significantly more expensive and harder to justify. Instead, decisions are being driven largely by safety concerns. The operational equivalent becomes long-term supply contracts with Atlantic Basin producers or acceptance of higher feedstock costs through finished product imports. Regional fuel distributors find their margin structure inverted storage capacity and inventory financing become profit centres as predictable supply access commands premium pricing from downstream customers.

Freight market dynamics reveal where margin concentrates during Persian Gulf disruptions. VLCC rates for alternative routes have surged: a West Africa to Asia voyage now earns approximately $35-40 per metric tonne versus $18-20/MT pre-conflict, with the premium accruing entirely to vessel operators rather than cargo owners. War risk premiums soaring 4,000 times higher than before the crisis mean that vessel owners with war risk coverage capture extraordinary daily rates for Strait transits up to $200,000 per day for modern VLCCs versus typical $25,000-35,000/day rates. The constraint lies in crew willingness and insurance availability rather than vessel capacity. Tanker operators with insurance relationships and experienced crew benefit from artificial scarcity pricing, while vessel owners dependent on spot coverage find themselves priced out of Persian Gulf business entirely.

Financing structures determine which operators survive margin compression during extended disruptions. Letters of credit (LCs) bank guarantees that payment will be made once shipping documents are presented become more restrictive when transit routes include war zones. In response to skyrocketing premiums and cancelled policies, the Trump administration directed the US International Development Finance Corporation (DFC) to provide political risk insurance to support continued shipping activity through the Strait of Hormuz. Banks now require additional documentation for Persian Gulf LCs: war risk insurance certificates, naval escort confirmations, and route specific approvals from flag state authorities. The operational result is that transaction timelines extend from standard 7-14 days to 30-45 days, forcing buyers to maintain higher working capital levels and sellers to accept longer payment cycles. Only traders with substantial credit facilities can absorb the financing gap.

The structural consequence extends beyond immediate disruption pricing into long-term infrastructure investment patterns. For Gulf exporters such as the UAE, the crisis has reinforced the strategic value of alternative export infrastructure, particularly the 1.5 million barrel per day Habshan–Fujairah pipeline, which enables shipments to bypass the Strait and maintain continuity of flows during maritime disruptions. Investment in pipeline capacity, storage infrastructure outside the Persian Gulf, and floating storage units becomes strategically essential rather than economically optional. The 2026 crisis demonstrates that geographic diversification of export infrastructure generates margin premiums that justify capital costs within single-disruption payback periods. Qatar's North Field South project now includes provisions for floating LNG storage in the Arabian Sea specifically to reduce Strait dependency.

Market structure shifts reveal which participants gain systematic advantage from persistent instability. Exporters with alternative routing capacity are better positioned to maintain market share during shipping disruptions and respond flexibly to tanker availability constraints and insurance cost spikes. The pricing benchmark system itself adapts: Fujairah delivered UAE crude trades at significant premiums to Persian Gulf pricing, creating a new benchmark structure that reflects transit optionality rather than crude quality differentials alone. Chinese strategic reserves benefit from inventory appreciation as stored Persian Gulf crude gains scarcity value. US shale producers operating in the Permian Basin capture enhanced margins as their production substitutes for constrained Middle Eastern supply, with WTI-Brent spreads widening to reflect transportation advantage rather than quality differences.

Insurance market evolution demonstrates how war risk pricing embeds permanently into regional trade costs. Insurers say reopening alone will not restore confidence unless it is followed by a sustained period without attacks, seizures or new mining incidents. Industry estimates suggest that premiums, which averaged about 0.25 per cent of vessel value before the conflict, have surged to between 3 per cent and 8 per cent, translating into insurance bills of $3 million to $8 million for a single large tanker transit. The new baseline reflects systematic reassessment of Persian Gulf risks: even after formal conflict resolution, war risk premiums are unlikely to return to pre-2026 levels given demonstrated infrastructure vulnerability. US defence officials estimate that clearing naval mines across the waterway could take up to six months, reflecting both operational complexity and uncertainty about the number and placement of explosives. Mine clearance represents the minimum requirement for insurance normalisation, but political risk assessment will permanently incorporate lessons from UAE-Iranian infrastructure targeting.

Central bank and strategic petroleum reserve (SPR) policies become primary margin determinants during extended disruptions. The US SPR release of 180 million barrels provides temporary price relief but depletes strategic buffers for future crises. China's SPR, estimated at 900 million barrels, offers Beijing flexibility to time purchases during price volatility while supporting preferred suppliers through guaranteed demand. US crude oil inventories fell for a sixth consecutive week, bringing stockpiles closer to minimum operating levels. The operational reality is that inventory draw downs can moderate price spikes temporarily, but sustained supply disruption eventually overwhelms strategic buffer capacity. Countries with larger strategic reserves gain relative economic advantage during prolonged crises through enhanced energy security and inventory management flexibility.

For procurement professionals monitoring Persian Gulf crude markets, the immediate signal is Brent-Dubai spread behaviour. The spread the price difference between North Sea Brent crude and Middle Eastern Dubai crude currently reflects a $8-12 per barrel premium for non-Persian Gulf supply. Historical norms suggest $2-4 spreads, meaning current levels embed sustained war risk expectations. The transit of ships through the strait is extremely scant and for it to become mainstream, it will require agreement on both the sides the US and Iran. Until the time there is a peace deal, we see reports of such transits as only exceptions. Monitor weekly fixture reports from Baltic Exchange for VLCC rates on benchmark routes: Middle East to Asia voyage rates above $50/MT indicate persistent supply constraint pricing, while rates below $30/MT suggest improving access conditions. The next 90 days will determine whether current disruption represents temporary crisis pricing or structural rebalancing of global crude oil trade flows.

.jpg)

.jpg)

'%3e%3cg id='Final-Copy-2_2_' transform='translate(1275.000000, 200.000000)'%3e%3cpath class='st0' d='M7.4,12.8h6.8l3.1-11.6H7.4C4.2,1.2,1.6,3.8,1.6,7S4.2,12.8,7.4,12.8z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3cg id='final---dec.11-2020'%3e%3cg id='_x30_208-our-toggle' transform='translate(-1275.000000, -200.000000)'%3e%3cg id='Final-Copy-2' transform='translate(1275.000000, 200.000000)'%3e%3cpath class='st1' d='M22.6,0H7.4c-3.9,0-7,3.1-7,7s3.1,7,7,7h15.2c3.9,0,7-3.1,7-7S26.4,0,22.6,0z M1.6,7c0-3.2,2.6-5.8,5.8-5.8 h9.9l-3.1,11.6H7.4C4.2,12.8,1.6,10.2,1.6,7z'/%3e%3cpath id='x' class='st2' d='M24.6,4c0.2,0.2,0.2,0.6,0,0.8l0,0L22.5,7l2.2,2.2c0.2,0.2,0.2,0.6,0,0.8c-0.2,0.2-0.6,0.2-0.8,0 l0,0l-2.2-2.2L19.5,10c-0.2,0.2-0.6,0.2-0.8,0c-0.2-0.2-0.2-0.6,0-0.8l0,0L20.8,7l-2.2-2.2c-0.2-0.2-0.2-0.6,0-0.8 c0.2-0.2,0.6-0.2,0.8,0l0,0l2.2,2.2L23.8,4C24,3.8,24.4,3.8,24.6,4z'/%3e%3cpath id='y' class='st3' d='M12.7,4.1c0.2,0.2,0.3,0.6,0.1,0.8l0,0L8.6,9.8C8.5,9.9,8.4,10,8.3,10c-0.2,0.1-0.5,0.1-0.7-0.1l0,0 L5.4,7.7c-0.2-0.2-0.2-0.6,0-0.8c0.2-0.2,0.6-0.2,0.8,0l0,0L8,8.6l3.8-4.5C12,3.9,12.4,3.9,12.7,4.1z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e) Privacy Choices

Privacy Choices